![[Translate to Englisch:]](/assets/group/_processed_/b/5/csm_Teaser_Monthly_V2_034ed09a63.png "[Translate to Englisch:]")

ESG criteria are steadily gaining in importance in the real estate market, especially when it comes to investment properties. Demand is rising for sustainable property solutions that are equally attractive, both environmentally and economically. Real estate projects that promote energy efficiency, make careful use of resources and offer healthy living spaces are finding increasing favour. This gives added weight to social aspects such as encouraging social integration and creating pleasant spaces for people to live in.

ESG is an omnipresent topic for real estate investors. They are committed to complying with the 2030 and 2050 climate targets of the Swiss Federal Council, which aim to reduce greenhouse gases over the long term in accordance with the Paris Climate Agreement. The legislator, of course, also sees itself as a driving force in the field. Apart from the regulatory requirements, other stakeholder groups in the real estate sector and institutional investors too are increasingly exerting pressure on real estate companies to incorporate ESG criteria into their strategies and processes, and develop and manage their property portfolios in a way that is climate-neutral and ESG-compliant.

The growing need for institutional investors to optimise their portfolios in terms of ESG has two consequences for their transaction activities. First, investigating the ESG criteria of properties being offered on the market is gaining importance in the due diligence process. Investors have joined forces with external consultants to design their own ESG measurement tools for application in due diligence reports. Simulations are also still done to assess the impact of a potential purchase on the previously defined reduction pathway of the investing vehicles and to formulate the measures that may be needed to ensure the new property will continue to make a positive contribution to the reduction pathway in the long term. These matters are also of key importance for the purchase process at SFP Group, and are assessed as part of a separate reporting process.

Another consequence is that properties which are not sustainable are increasingly being put up for sale. Over the past few years we have seen a steady increase in the share of properties offered that are not sustainable.

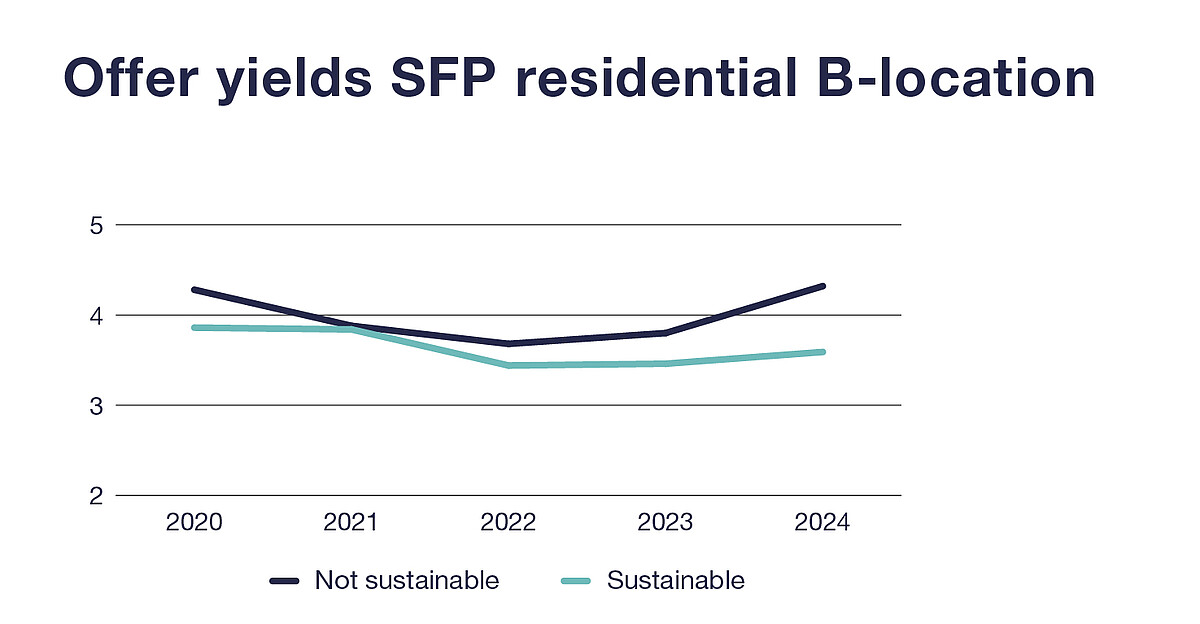

Source: Swiss Finance & Property Group, 2024

Since 2021 the share of properties offered to us that are not sustainable has exceeded 50% of the entire volume on offer. At the same time, the share of as-new properties has dropped from a high of 42% in 2020 to just 19% in 2023. We expect to see a further drop in the share of properties in mint condition in 2024.

Combined with the preference institutional investors have for buying such properties, this decline in the availability of as-new and therefore sustainable properties has affected the returns earned on properties in the transactions we monitor. The trend has also affected demand for, and hence also returns on, properties that are not sustainable.

Source: Swiss Finance & Property Group, 2024

Viewed in isolation, the change in demand should now result in a “green premium” for sustainable properties, or a “brown discount” for ones that are not. However, right in the middle of this development interest rates changed direction in 2022, which theoretically should have led to falling prices for all properties. But based on what we can conclude from our own willingness to pay and the transactions we have monitored, yields have stagnated on sustainable properties and increased for properties that are not sustainable. The result is a noticeable spread between the two types of properties, and therefore a clearly discernible “brown price discount”.

As institutional investors represented an important buyer group in the real estate market until interest rates changed direction, their lack of interest in particular in buying properties that are not sustainable necessarily requires adjustments to the process of selling them. As mentioned before, many institutional investors nowadays are increasingly considering selling smaller and older properties in order to bundle together their capacities to carry out ESG-driven refurbishments of larger properties. Although private investors have partly absorbed this excess, their willingness to pay is very different, not least because banks are intensifying their focus on the sustainability of the properties they finance when approving mortgages. In trying to sell these properties, it is crucial to be well acquainted with this investor group and able to meet their requirements. A two-stage bidding process can often be daunting to such investors. To sell properties which are not sustainable at attractive prices and within a reasonable period in the current market environment, it must be possible to offer them a degree of certainty that a transaction will take place, by restricting the number of possible investors. This raises the question of whether the two-stage bidding process which has become almost standard in recent years is still the correct choice for these assets.

It is clear that the real estate market is undergoing a period of change due to higher sustainability requirements, a situation exacerbated by the interest rate turnaround. Investors have to adapt quickly to the change in circumstances if they wish to exploit the opportunities and possibilities arising.

Authors